FY 2020

Kinsman Oak Investor Letter FY 2020

February 3, 2021

KEY TAKEAWAYS

We strive to continuously optimize our internal process in the pursuit of maximizing alpha. This optimization process is iterative and requires constant re-evaluation of how we select stocks and construct the portfolio. Even small incremental changes will reap meaningful benefits as marginal gains compound over time. Below are a few key takeaways from the past year.

Our Highest Conviction Ideas Did Best

Gains were most significant amongst our largest weights. Stocks in the bottom half of the portfolio underperformed those in the top half and did not contribute much in the way of diversification. This is unsurprising as correlations in general were quite high. It was a small sample size but if this trend continues, the Fund may lean towards the more concentrated range of our mandate in the future.

Focusing on Bottom-Up Stock Picking Drives Performance

The best performing stocks in the portfolio were selected due to company-specific characteristics. Identifying opportunities with idiosyncratic prospective return profiles is time consuming. Our limited hours are best spent tirelessly turning over as many rocks as possible looking for needles in haystacks rather than reading about macroeconomic factors that provide little actionable value.

Heightened Volatility Tests an Investor’s Conviction in the Thesis

At times, it was difficult to distinguish temporary price volatility (noise) from price movements related to changing fundamentals (signals). Rotation trades and re-normalization rips created choppy market conditions. Companies pulled forward guidance and investors had little visibility into underlying business performance. Having deep conviction in an investment thesis mitigates the risk of being whipsawed or shaken out of positions due to elevated levels of noise. Volatility creates opportunity for patient investors and sizing positions correctly provides the flexibility to take advantage of interim price swings. We believe a higher volatility regime is only beginning and we look forward to the challenges and the opportunities that presents going forward.

REVIEW OF 2020 AND PREVIEW OF 2021

Investors entered the year on autopilot when everything was turned upside down rather quickly. A sharp correction was met with an unprecedented policy response and markets never looked back. The Fed Put metastasized into a Government Put and the psychological pendulum swung from peak pandemonium to peak euphoria within months. It appears we may have finally reached the limit of monetary policy efficacy and increased reliance on fiscal spending will be the norm going forward.

Market participants became more emboldened as the year progressed once it became clear policy makers would stop at nothing to keep financial assets from going down. A speculative mania ensued as the fear of missing out displaced the fear of losing money. This frenzy, unrivalled in terms of its breadth, shows no signs of abating anytime soon as reckless risk-taking has only continued to intensify so far this year.

Central bank intervention distorts asset prices on its own, and this kind of manic investor behaviour amplifies the amount of noise. The combination makes it exceedingly difficult to discern market signals and true price discovery. Fractional ownership stakes in real businesses have been reduced to get-rich-quick vehicles for investors, check boxes on political scorecards, and to serve as a barometer for how much The Fed needs to dial up its accommodative measures (because there is no dialing it back now).

We believe conditions today share striking similarities to the dot-com era. Valuations are severely overextended while the appetite for risk-taking is the highest it has been since 1999. We could show you numerous charts and graphs to support our view that prices today would be considered nosebleed valuations in any historical context, but we do not see the point of reiterating the same content you see elsewhere.

Suffice it to say, investors are relying on a never-ending supply of monetary accommodation and permanent real ZIRP to justify current valuations. Extrapolating anything indefinitely is asking for trouble, especially in the realm of economics where the future is wildly unpredictable. Even if omnipotent central banks could prevent negative outcomes until the end of time, starting valuations if you were to buy stocks today would practically guarantee a low expected rate of return on equities over the coming years.

It’s worth noting overvaluation is pervasive throughout the market and is not only confined to a handful of large-cap stocks. Median multiples are excessive across all market capitalizations and most sectors. Ultra-low interest rates are often used as a reason to justify higher valuation multiples while the corresponding ultra-low real GDP growth rates they cause are largely ignored.

From a sentiment perspective, everybody is looking for a reason to be bullish. Good news is good news and bad news is spun to fit a bullish narrative anyways. Like the progression of the dot-com bubble, investor enthusiasm has progressively shifted away from dominant high-quality companies to less established start-up companies with large total addressable markets but minimal, if any, legitimacy. We have the lowest put-to-call ratio, the highest small trader call option volume, the largest amount margin debt outstanding, and an explosion in retail participation.

The market is inhospitable to bears and short sellers. Current short interest is close to record lows as many participants have opted to throw in the towel. After all, if central banks are determined to send stocks higher en masse, why bother swimming against such a strong current? Funds that decided to maintain short positions may have found themselves on the wrong end of a short squeeze and/or gamma squeeze orchestrated by coordinated groups of retail investors. A basket of heavily shorted stocks has significantly outperformed broad indexes year-to-date (Appendix A) and speaks volumes to current market sentiment.

Investors are beginning to accept the notion large swathes of the market are firmly in bubble territory. We were early in raising our concerns, but it appears the rising speculative fervor is becoming increasingly difficult for others to ignore. Spotting bubbles is easy, navigating them is more challenging, and calling the top is impossible. If we are correct in our assertion that facets of this market are experiencing bubble-like characteristics, assessing systemic risk from the fallout cannot be done.

Herein lies the existential question: Is risk even worth paying attention to anymore? A global pandemic shuttered economic activity overnight, unemployment spiked to Great Depression levels, and circuit breakers constantly halted trading last March. Despite all the carnage, this dip turned out to be one of the greatest buying opportunities of a lifetime. If you were able to close your eyes and remain invested, you probably came out unscathed within six months and made money by year end. Policy makers have reinforced the idea that the only thing to fear is fear itself, and if you remain invested, no matter the circumstances, you will be made whole.

But the notion that policy makers will unconditionally have your back may prove to be incorrect at precisely the time when it is needed most. The faulty critical assumption embedded in this belief is that policy makers are willing and able to have your back at all times. In our opinion, believing this requires a gigantic leap of faith we are not comfortable making. We can envision a scenario where, despite best efforts, monetary and fiscal measures fail to have the desired effects on financial markets. As such, our answer to the existential question posed above is yes. We believe risk is always worth paying attention to.

The more immediate question is: Where do we go from here? We entered 2021 with infinite monetary policy accommodation, seemingly limitless fiscal stimulus, and the optics of strong sequential growth metrics for companies in most sectors. But everybody already knows this and the bull case from here disregards valuation multiples almost entirely. Sentiment-based warning signals are flashing red but fundamental warning signs are not there yet. We have explored this bizarre dichotomy in depth elsewhere and do not want to rehash it here.

While the existence of an asset bubble appears likely, proximate causes for its bursting do not yet appear imminent. Bubble tops are commonly preceded by central bank tightening and rolling over fundamental indicators. We don’t envision a scenario where monetary or fiscal support is meaningfully withdrawn regardless of what happens to asset prices or inflation. We believe this cycle is destined to eventually culminate in a blow-off top.

Halfway through this year people will begin to look forward to 2022. For better or worse, reality will eventually reassert itself. The expectation of pent-up demand is embedded in prices. Labour market conditions are a big question mark and the propensity to save may be much higher than the market anticipates. Transitory reflation could ultimately give way to stronger structural deflationary forces.

Animal spirits can drive excesses over long stretches of time, but eventually stock prices will approximately reflect their intrinsic value. If past cycles have taught us anything, it’s that excesses can persist for far longer than people think. Further, just because certain pockets may be in bubble territory, it doesn’t mean every publicly traded security is overvalued. We feel a lot of opportunity exists despite our belief that excessive froth permeates many areas of the market.

WHERE WE SEE FROTH

While much ado is made about FAANGM valuations in the financial media, we believe four other areas will prove to be more troublesome over the coming years. In our view, the biggest dislocations between stock price and fair value are concentrated in the following pockets. The first two encapsulate how the fear of missing out has escalated into you only live once. The following two are comprised of real businesses whose valuations are pricing in too much optimism.

Short Squeeze Bubble

GameStop (GME) is the poster child for this basket. To sum it up briefly, a group of investors/retail traders targeted heavily shorted stocks and attempted to create a short squeeze/gamma squeeze by purchasing large amounts of shares and out of the money call options. A self-reinforcing process pushes shares higher and higher as short sellers are forced to cover and market makers buy shares to hedge the call option writing. Although GameStop has received the most attention, this kind of dynamic was not confined to only one stock. Other examples are listed in Appendix B.

Greater Fool Bubble

Under normal market conditions, the constituents of this basket would generally be considered productive hunting grounds for short opportunities. Many could also be included in the short squeeze bubble category. These businesses tend to have smaller market caps and are highly speculative. Included in this group would be overvalued SPACs, “electric vehicle” businesses with limited operating histories, dubious Chinese-listed companies, and the like.

These stocks have performed well and garner a lot of social media hype as inexperienced investors gamble with their stimulus checks and encourage others to do the same. Examples include Nikola Corporation (NKLA), Blink Charging (BLNK), Plug Power (PLUG), Luminar Technologies (LAZR), etc. But at some point, the market will run out of greater fools. Collectively, shares in this group could drop in value by more than 90% without any noticeable ramifications for the broader market.

TAM Narrative Bubble

GAAP means Growth At Any Price for businesses with large TAMs and compelling narratives. We believe expensive software companies trading between 30x-200x forward revenues will significantly underperform the market over the next ten years. Companies in this frothy pocket are emblematic of a market that is price insensitive for growth. It is impossible to justify owning these stocks with any semblance of valuation discipline, even if there are winner-take-all dynamics at play. Paying $50 for $1 worth of sales while the company loses money is a difficult valuation to ever grow into, no matter how large the TAM is and regardless of how well the business executes.

Even worse, the TAM bubble has progressed beyond high-quality software companies with high margins, network effects, recurring revenues, etc. to a subset of narrative stocks disguised as great businesses. These posers possess none of the same valuable characteristics but instead tout negative unit economics, low switching costs, minimal barriers to entry, and barely any scale benefits. But for now, this group of stocks can continue rising as very expensive may become very, very, very expensive.

Re-Opening Euphoria

The vaccine development and subsequent rollout has fueled a lot of optimism for businesses geared towards the re-opening trade. We understand why but feel many stocks have experienced strong rallies that far exceed the expected fundamental improvements. At this point, valuations leave very little room for further gains. We have compiled a list of stocks in Appendix C and compare pre-virus EBITDA expectations to current EBITDA expectations. The average FY22 estimate has declined by 8% while the average stock price has increased by 32%. The delta between the change in expectations and the change in stock price is jarring, in our view, and we question how much more upside, if any, these stocks have.

For instance, the Russell 2000 lost $1.02 trillion worth of market cap from peak to trough in early 2020, but has since gained $1.77 trillion, way overshooting prior highs (Appendix D). The index’s market cap is ~30% higher today despite a deteriorating two-year growth outlook when compared to pre-virus expectations. Even if investors are prepared to look beyond short-term uncertainty, valuations reflect all kinds of sunshine and rainbows at other side of the tunnel. Value and re-opening are not synonymous terms. Most of these businesses are simply not cheap on an absolute or relative basis.

WHERE WE SEE OPPORTUNITY

From a stock picker’s perspective, we see a lot of opportunity investing in off the beaten path ideas, where we find most of our success, and two large cap tech stocks we believe are relative bargains hiding in plain sight. From a bigger picture perspective, we are optimistic about the future of active management.

Off the Beaten Path Ideas

The rising tide eliminated low-hanging fruit where broad sectors or sub-sectors could have been blatantly undervalued. Everything that remains cheap now is cheap for a reason. Instead, we are finding company-specific opportunities on the long side which should possess an idiosyncratic return profile. Positive needle-moving fundamental developments can provide substantial upside in the intermediate term, regardless of what the broader market does. Negative developments will have the opposite effect. These stocks tend to have smaller market caps, and are generally underappreciated, neglected, or misunderstood.

Two Large Cap Tech Stocks

Our view on Alphabet (GOOG) and Facebook (FB) may be somewhat controversial. The bear case for both boils down to antitrust risk and valuation. Our thesis is predicated on the belief that real earnings power, especially for Alphabet, is higher than it appears on the surface. At first glance, Alphabet’s P/E appears to be 30.2x. Adjusting for net cash brings this down to 27.9x. Alphabet’s “Other Bets” segment generates de minimis revenues but reduces operating income by 13%. Adjusting for that (and assigning zero value to a segment that includes Waymo, Nest, and Verily) brings the multiple to 24.7x versus the S&P 500 trading at 22.3x.

Alphabet, at a 10% premium to the S&P 500, is one of the biggest relative value bargains hiding in plain sight we have seen. Alphabet has a much deeper moat, better margin profile, less capex requirements, and faster growth profile than the average company within the index (estimated 18% CAGR for the next two years versus 8% for the S&P 500).

Pushing the envelope, Alphabet’s multiple would be lower than the overall market if the company treated stock-based compensation as dilution and/or if research & development was capitalized instead of expensed. Internally we use a more detailed sum-of-the-parts analysis to more closely approximate intrinsic value. Further, Waymo provides significant upside optionality, especially if you believe Tesla’s “full self driving” technology justifies a large portion of its market cap.

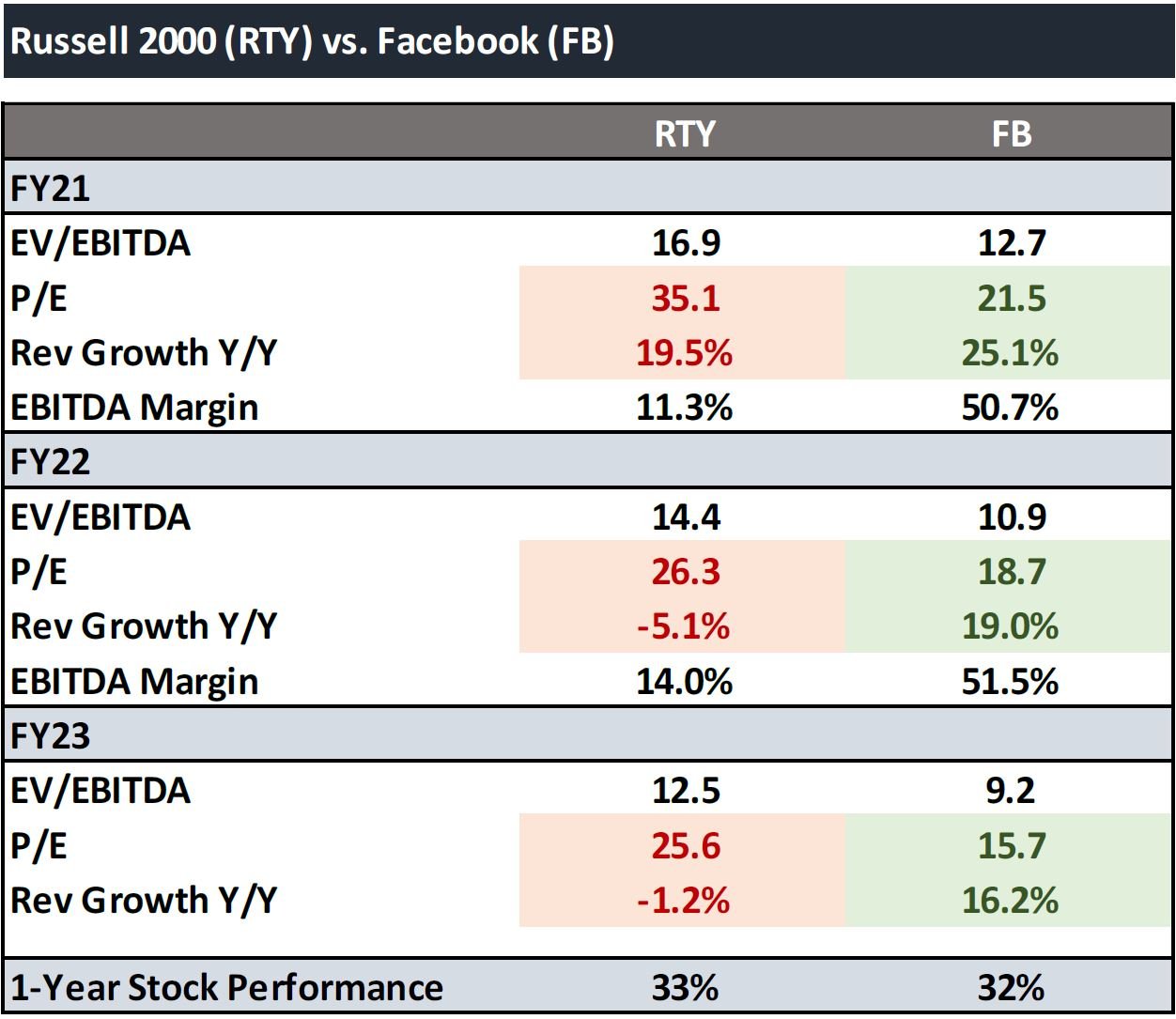

Facebook, although to a lesser degree, is a relative value bargain as well. We believe the company possesses an element of platform risk that Alphabet does not but, compared to the rest of the market, the stock still seems undervalued. We compared Facebook to the Russell 2000, an index full of cyclical businesses that are considered no-brainers at the beginning of a recovery and popular re-opening stocks that are poised to go higher after the vaccine is distributed (Appendix E). Facebook is significantly cheaper, growing faster, has a larger economic moat, superior margin profile, and requires less capex.

In short, we believe the obfuscated earnings power makes Alphabet and Facebook appear more expensive than they really are. After adjusting for factors like “Other Bets” in Alphabet’s case or net cash, stock-based compensation, and research and development treatment for both, it becomes clear that investors are being adequately compensated for the associated antitrust and regulatory risk.

Pent-Up Dispersion

We hear a lot about pent-up demand, but we are far more excited about pent-up dispersion. Stocks have spent the past year trading in baskets based on narratives, headlines, and momentum. Correlation was high between groups of stocks depending on their sensitivity to the pandemic. For instance, there was little dispersion within the liquidity beneficiaries basket, the stay-at-home basket, and the re-opening basket. Companies that didn’t deserve to rally did so, and companies that deserved to rally more didn’t rally enough. The constituents traded in unison irrespective of underlying fundamentals.

We expect the dichotomy between winners and losers to be accentuated as economic conditions begin to normalize. Some companies will emerge as structurally improved market share gainers while others will emerge weaker and more indebted. It remains to be seen whether COVID-19 beneficiaries will continue to experience tailwinds from an acceleration of a pre-existing secular trend or if increased sales were a one-time mean-reverting bump that pulled forward demand from future periods. A potential black hole of demand potentially awaits companies that fit the latter.

Elevated valuations are a pull forward of future returns, the same way excessive debt is a pull forward of future demand. Expensive beginning valuations essentially guarantee below average long-term returns. But while markets may have low returns going forward, the right stocks won’t. Increased dispersion of underlying fundamentals should provide tailwinds to active management, offsetting some of the headwinds from a continued shift to passive investment vehicles.

Accelerating Pace of Innovation

The pace of innovation is continuing to accelerate which creates a lot of opportunities to identify potential winners. On top of that, more sectors are experiencing a winner take all dynamic which can present interesting opportunities provided the stocks are not wildly overpriced. Many businesses in the TAM Narrative Bubble referenced above fit this description and we may look to initiate positions if valuations multiples suddenly contract.

Survival of the Biggest

Industry leaders are increasingly becoming market share gainers. The pandemic and the associated lockdown measures disproportionately impacted smaller businesses. Companies without excess liquidity, access to cheap credit, or scale benefits likely lost significant share to larger competitors who had those things. This dynamic could potentially drive consolidation in some industries and will almost certainly result in a more concentrated competitive landscape either way. In short, the big will get bigger.

When It Rains, It Pours

An accelerated pace of innovation combined with an increasingly fierce competitive landscape puts second and third tier players in an incredibly disadvantageous position. These businesses are already losing share to larger traditional competitors. At the same time, they will likely cede additional market share as new, more innovative, entrants encroach on their turf. While these stocks may screen cheap, we would suggest exercising caution. Shrinking revenues, an abruptly deteriorating economic moat, and high operating leverage are the ingredients for a perfect storm.

LOOKING BEYOND 2021

We do not believe we are in the early stages of a new bull market given the brevity of last year’s decline and rally. Healthy bottoming out processes that mark the end of one cycle and the beginning of another take time. A certain degree of cleansing is required to address the misallocation of capital that occurs during the eight and ninth inning of the prior bull market. As such, we feel it is more likely we are still in the same cycle as we were one year ago.

Assessing the strength of the economic recovery is difficult to gauge with unprecedented monetary easing and fiscal largess clouding underlying indicators. It is bad enough these measures distort asset prices but, even worse, they obfuscate important warnings signals. We wonder how robust this recovery really is if the Fed believes even thinking about thinking about raising rates will cause it all to unwind. If economic function requires continuous life support from ultra-low artificial interest rates and ever-increasing fiscal deficits, can it ever truly recover and stand on its own two feet?

Longer-term, the outlook depends on how the economy performs after the effects of the pandemic subside. The economy may benefit from temporary pent-up demand but, upon normalization, it will be saddled with a larger debt overhang, lower interest rates, and less creative destruction. All of which point to structurally lower real GDP growth, like Japan and Europe. We wrote about the lost decade for equities in our launch letter and our conviction in this thesis has increased since we first discussed it.

The upward trajectory of the stock market masks its inherent fragility and valuations remain expensive. A black swan-level event is no longer required for something catastrophic to happen. As such, we believe the way forward involves tighter risk management and using interim volatility to our advantage.

Each subsequent policy response to economic turbulence is exponentially greater than the one preceding it. The magnitude of monetary easing and fiscal stimulus during the next crisis will make current measures look like a warm-up, the same way we think about past policy responses compared to today. Central banks find themselves on an unsustainable treadmill, stuck in a debt trap, that we can no longer grow our way out of. Eventually, the only two options will be deflationary defaults or inflating it away.

Comparing the speculative fervor today to the dot-com era may seem overly pessimistic but it is worth noting active stock picking and value investing in general performed well for many years post-bust. Perhaps this is wishful thinking on our part, and we recognize valuations are not as cheap today as they were back then, but we see an opportunity for active managers to add value.

Further, in a world of zero percent real yields, there is simply nowhere else to be invested. We see no viable alternative to owning equities and other risk assets at this juncture. As such, we continue to deploy capital opportunistically into specific securities we feel will experience an idiosyncratic return profile, while being cognizant of potential looming market risks on the horizon.

Sincerely,